इस पोस्ट में क्या है ?

What is a Crossed Cheque

Crossing of Cheque: The open cheques are presented by the payee to the banker on whom they are drawn and are paid over the counter. It is obvious that an open cheque is liable to great risk in the course of circulation. It may be stolen or lost, and the finder can get it cashed, unless the drawer has already countermanded payment. In order to avoid the losses incurred by open cheques getting into the hands of wrong parties, the custom of crossing of cheques was introduced. You can delve into the Crossing Of Cheque meaning and explore the various types of crossing of cheques that enhance the security of financial transactions.

Crossing Of Cheque Meaning

Crossing Of Cheque Meaning A crossed cheque is essentially a cheque marked with two parallel lines, either across the entire cheque or in the top-left corner. This marking signifies that the cheque can only be deposited directly into a bank account and cannot be immediately cashed by a bank or any other credit institution. This measure provides an additional layer of security for the payer, as it requires the funds to be processed through a collecting bank.

Why Cross a Cheque?

Crossing a cheque provides specific instructions to financial institutions on how to handle the funds. Crossed cheques are typically identified by two parallel lines drawn vertically across the cheque or at the top left-hand corner. Between these lines, additional wording like ‘and company’ or ‘not negotiable’ may be included. However, merely drawing the lines without any added text does not change the meaning of the crossed cheque. Crossed cheques are used by cheque writers to safeguard the transmitted amount from being cashed by an unauthorized person or from being stolen. The format and regulations surrounding crossed cheques may vary among different countries. Since crossed cheques can only be processed through a bank account, the recipient’s transaction record can be traced for future reference and clarifications.

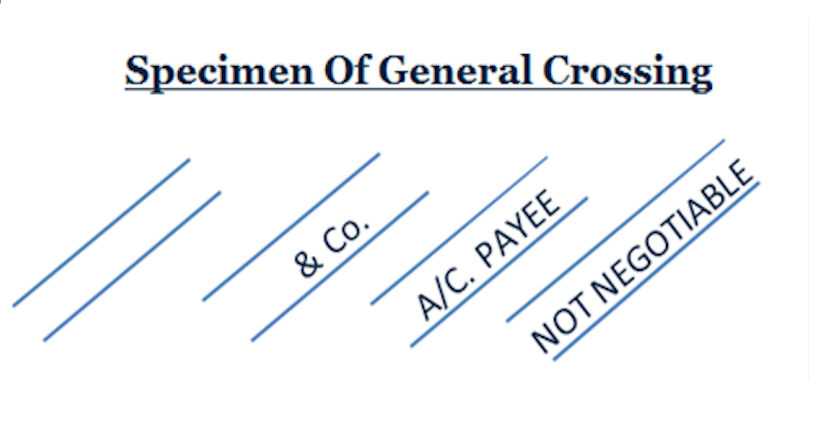

Various Ways to Cross a Cheque

Crossing a cheque focuses on the instructions provided by the drawer (the person issuing the cheque) to the drawee bank (the bank on which the cheque is drawn). The instructions dictate that the cheque must be paid at the bank’s counter, with strict instructions to pay it to a person who presents it through a banker. There are various types of cheque crossing to secure payments:

- General Crossing: This type of cheque crossing consists of two parallel transverse lines, which can be placed anywhere on the cheque, though it is often recommended to position them in the top-left corner. The main purpose is to ensure that the cheque must be paid to the bank.

- Account Payee Crossing: Also known as restrictive crossing, this type of cheque must include the words “account payee” or “account payee only.” The cheque can be crossed either generally or specifically, and it signifies that the cheque is no longer negotiable.

- Special Crossing: This type of cheque crossing does not require the name of the banker. The effect of this crossing is that the cheque must be paid only to the specified banker it is crossed to. It serves as a reminder that a special crossing cannot be changed into a general crossing.

- Not Negotiable Crossing: In this type of cheque crossing, the words “not negotiable” must be included. The cheque can be crossed either generally or specifically, and it remains non-negotiable. The title of the transferee will not be better than the title of the transferor.

Uncrossing the Cheque

Once a cheque is crossed, the payee cannot uncross it. Moreover, the cheque is considered non-transferable, meaning it cannot be transferred to a third party. The only permitted action is for the payee to deposit the cheque into their own account. Attempting to uncross the cheque by marking “crossing cancelled” on the front side is discouraged, as it removes the protection initially provided by the payer.

Frequently Asked Questions (FAQ)

A crossed cheque is a type of cheque marked with two parallel lines, either across the entire cheque or in the top-left corner. This marking indicates that the cheque can only be deposited directly into a bank account and cannot be immediately cashed.

A cheque is crossed to provide specific instructions to financial institutions on how to handle the funds. It enhances security by ensuring that the funds are processed through a collecting bank and not immediately cashed.

There are several types of cheque crossing, including general crossing, account payee crossing, special crossing, and not negotiable crossing. Each type serves different purposes and provides specific instructions.

Once a cheque is crossed, it cannot be uncrossed. The payee is required to deposit the cheque into their own bank account. Any attempt to uncross the cheque by marking “crossing cancelled” is discouraged.

Crossing is used to secure cheque payments and prevent unauthorized individuals from cashing the cheque. It ensures that the funds are processed through a bank account, allowing for traceability.